Friends, if you’re thinking of buying your first dream home in big cities like Mumbai or Pune, then the question “How to apply for PMAY with MHADA Lottery” is the most important one for you. Under the Pradhan Mantri Awas Yojana (PMAY), first-time homebuyers receive a subsidy ranging from ₹2.5 lakh to ₹2.67 lakh.

Let’s say you get a ₹30 lakh house in the MHADA lottery. And if you are eligible for PMAY, your actual cost will be directly reduced because the government itself pays a portion of your loan. But remember, this subsidy is only for those who do not own a “Pucca House,” i.e., a permanent house, anywhere in the country.

What is the connection between PMAY and MHADA?

Many people get confused about whether PMAY and MHADA are separate. But there’s no need to be confused. In fact, MHADA is an agency that builds houses, and PMAY is a government of India scheme that provides subsidies. In many MHADA lotteries, “PMAY Units” are reserved.

When you fill out the MHADA form, there’s an option that asks, “Do you want to apply under PMAY?” If you select “Yes,” you must provide your PMAY Registration Certificate. This gives you two major benefits:

- Lower Interest Rate: The interest rate on the loan you take from the bank is reduced.

- Direct Subsidy: An amount of up to ₹2.5 lakh is deducted from your loan principal amount.

Eligibility: Who Can Take Advantage of PMAY or MHADA?

According to MHADA rules and PMAY guidelines, you are only eligible if:

- First Home: You or any member of your family such as your spouse or unmarried children must not own a pucca house anywhere in India.

- Income Slabs: Your annual family income must be between ₹3 lakh and ₹6 lakh (EWS/LIG category). (Note: CLSS subsidy rules for MIG changed in 2026, please check them once).

- Aadhaar Linking: Your Aadhaar card must be linked to your mobile number.

Step-by-Step: How to Apply for PMAY with MHADA Lottery Online

If you haven’t registered for PMAY-U 2.0 yet, follow the steps below carefully:

Step 1: Visit the PMAY Official Portal

First, visit the PMAY-U 2.0 Official Website and you will see an “Apply for PMAY-U 2.0” button. As soon as you click on it, it will redirect you to another authorized website.

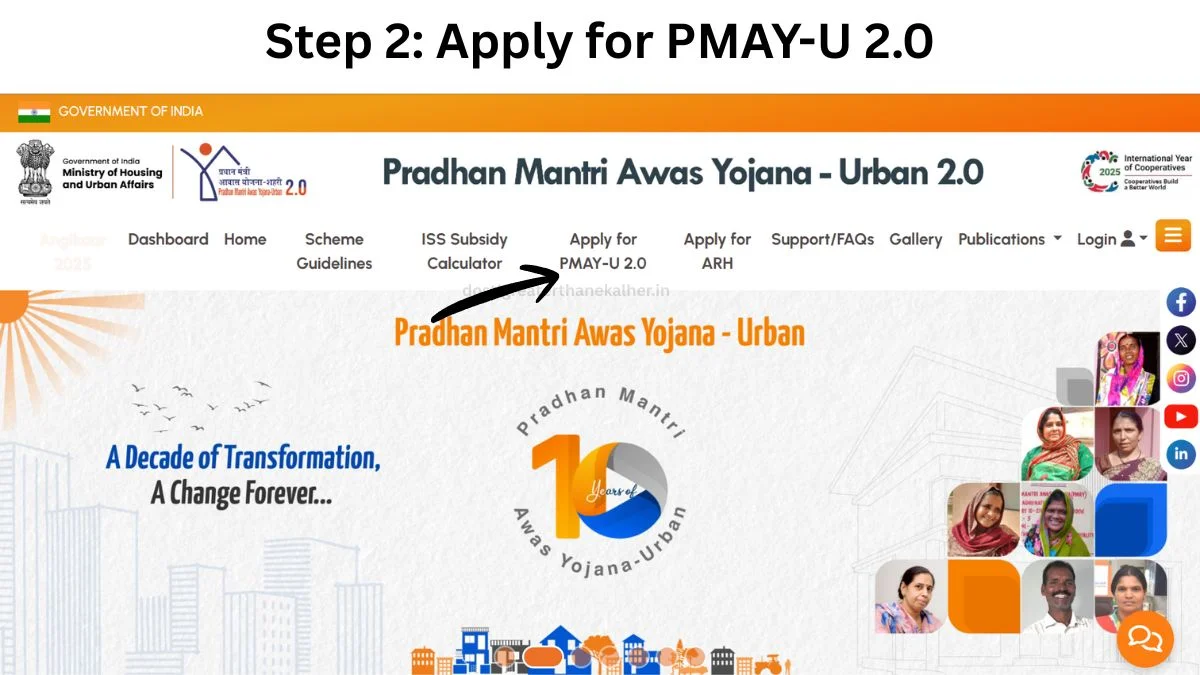

Step 2: Apply for PMAY-U 2.0

On the website’s home page, you will see many options; you need to click on “Apply for PMAY-U 2.0.” After that, you must carefully read the information provided on the portal and then proceed.

Step 3: User Authentication (Mobile & Aadhaar)

Compared to before, authentication has become much stricter. For this, you will need to:

-First, enter your mobile number and captcha to generate an OTP.

-After logging in, you will need to enter your Aadhaar Number. This will be verified directly to check if you are already receiving any PMAY benefits.

Step 4: Component Selection (Verticals)

You will see 4 options, but for the MHADA lottery, you have to choose one of them:

-Interest Subsidy Scheme (ISS): If you want a subsidy on a bank loan (Most MHADA winners choose this).

-Affordable Housing in Partnership (AHP): If you are specifically applying for MHADA’s PMAY flats.

Step 4: Assessment ID Generation

After filling in all the details (Income, Address, Family details) and clicking Save, you will receive a 17-digit Assessment ID. This is the ID you need to enter in the ‘PMAY Registration Number’ field on the MHADA form.

PMAY Subsidy Calculation: How Much Money Will You Get Back?

Friends, the biggest attraction of PMAY is its interest subsidy model. This doesn’t mean the government will give you cash; rather, the government pays a portion of your loan itself, which significantly reduces your EMI.

According to the PMAY 2.0 rules in 2026, the subsidy amount depends on your income group. You can easily understand this from the table below:

| Category | Annual Income Slab | Max Loan for Subsidy | Subsidy Amount (Approx) |

| EWS | Up to ₹3 Lakh | ₹6 Lakh | ₹2.50 Lakh – ₹2.67 Lakh |

| LIG | ₹3 Lakh – ₹6 Lakh | ₹6 Lakh | ₹2.30 Lakh – ₹2.50 Lakh |

| MIG | ₹6 Lakh – ₹9 Lakh | ₹9 Lakh | Up to ₹1.80 Lakh |

Please note: If you take a ₹30 lakh loan, the subsidy applies only to the first ₹6 lakh (EWS/LIG) or ₹9 lakh (MIG). You have to pay normal bank interest on the remaining loan amount.

Important Documents: Checklist for the PMAY-MHADA Application

When you are preparing to fill out the form, be sure to have these documents scanned and ready. If even one document is missing, your subsidy process may be delayed:

- Aadhaar Card: For both the husband and wife (Mandatory).

- PAN Card: For income verification.

- PMAY Registration Certificate: The one you downloaded from the PMAY portal.

- Self-Declaration Affidavit: To declare that you do not own another pucca house anywhere in India.

- Income Proof: ITR for the last 3 years or an Income Certificate issued by the Tehsildar.

- Caste Certificate: This document is very important if you are applying from a reserved category.

Common Mistakes: Why is the PMAY Subsidy Rejected?

I have seen that even after being selected in the lottery, many people’s subsidies get rejected. This is because they make these 3 mistakes, which you should definitely avoid:

- Name Mismatch: Your name must be exactly the same on your Aadhaar, PAN, and MHADA application. If you’ve written “Suresh Kumar” on the MHADA form but your documents show “Suresh Kumar Gupta,” your subsidy could be held up. Therefore, fill in your name carefully.

- Property Ownership: If your spouse or unmarried children own a house anywhere in the country, do not apply. The subsidy will be canceled if you are caught during verification.

- Wrong Income Category: If your income is ₹7 Lakh and you have applied under EWS (Up to ₹3-6 Lakh), you will be disqualified.

Conclusion: Take advantage of the subsidy today.

Friends, the process of applying for PMAY through the MHADA lottery may seem a bit technical, but saving ₹2.5 lakh can be a huge relief for you. Just keep your documents ready and be sure to double-check the details when linking.

Frequently Asked Questions

Can I get the PMAY subsidy without a bank loan?

No, the PMAY-CLSS subsidy is only available when you take a home loan from a bank. If you are buying a house with cash, then this subsidy will not apply.

When does the subsidy come to the bank account?

After the lottery is drawn and the loan is sanctioned, the bank sends your data to the NHB (National Housing Bank). After verification, the subsidy is credited to your loan account within 3 to 6 months.

Can an unmarried adult child apply separately?

Yes, if the child is an adult (18+) and earns, they are considered a separate “Family,” even if their parents own a home.

What is the difference between PMAY 2.0 and the old PMAY?

In PMAY 2.0 (2026), the income slabs and property value caps (Up to ₹35 Lakh) have been slightly updated so that more urban middle-class people can benefit.

Disclaimer: This information is based on the PMAY 2.0 guidelines. The final subsidy decision depends on verification by the National Housing Bank (NHB) and MHADA. Before applying, be sure to check their exact rules on the official PMAY portal.